Education Service Units Property Tax Relief

Nebraskans want property tax relief, and lawmakers continue to seek options to deliver tax relief without fueling local government overspending. And unlike in the flush revenue years of 2021-2023, lawmakers also face tightening budgets in upcoming fiscal years.

One option for property tax relief is to continue removing smaller property tax levies altogether. For example, Nebraska enacted legislation in 2023 to eliminate community college property taxes. State funds will be used to replace the community college property tax, resulting in a $300 million reduction in property taxes and a simplified property tax bill.

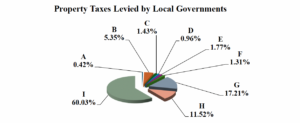

Lawmakers can consider a similar approach to Education Service Units (ESUs) to provide tangible property tax relief. LB 389, sponsored by Senator Dave Murman, would eliminate the property tax for educational services units (ESUs) starting in fiscal year 2028-2029, and replace that funding with state funds. The estimated state cost is $65 million per year in FY 2031. ESU property taxes currently account for 1% of the property tax burden, while community colleges accounted for 5.5% of the property tax burden (currently 1.77%). The community college property tax is currently being phased out.

Suppose the state has $65 million to use for property tax relief. What would be the best way to “put lead on target” to deliver tax relief for homeowners? In one option, the ESU property tax could be eliminated, resulting in exactly $65 million in lower property taxes and a simpler tax bill. Alternatively, lawmakers can provide an additional $65 million to K-12 schools and hope school districts would apply the funding to property tax relief. As lawmakers have already learned, some districts will provide tax relief, and others will not. The only way to guarantee $65 million in property tax relief is to eliminate the entire ESU tax, which will provide relief to all ESU districts across the state.

For the last 5 years, Nebraska has leveraged state funds to reduce local property taxes through programs such as the LB 1107 credits and through providing new funding to local governments in the hope that they will provide property tax relief. However, these efforts have not completely succeeded. Hundreds of millions of dollars in credits to offset property taxes have been left unclaimed in the state treasury. In addition, new state funding to offset local property taxes do not always result in dollar-for-dollar property tax relief because local governments do not necessary deploy new state funds for property tax relief.

The elimination of community college property taxes is one exception to this trend. In 2024, Nebraska enacted legislation to use state funding to fully replace the property tax portion of community college funding. This will result in roughly $300 million of direct property tax relief when the community college property tax goes away entirely.

Nebraska’s property tax ranks 45th in the nation for overall competitiveness, according to the Tax Foundation’s state competitiveness rankings. High tax rates are a big reason for Nebraska’s ranking, and tax credits do not provide the same relief as lower levies.

The community college model can be applied to ESUs to deliver direct property tax relief and a simpler property tax bill. Thus, LB 389 creates a viable pathway for direct property tax relief modeled upon the success of eliminating community college property taxes. ESUs can even be granted a “safe harbor” protection that will allow them to levy property taxes if the state every comes up short on required funding, as has been granted to community colleges. Given tighter state finances and the need for tangible property tax relief, repealing ESU property taxes is a strong option for lawmakers to advance.