Discriminatory Taxes Make Unreliable Revenue Sources

As Nebraska lawmakers work to close a revenue gap and consider additional property tax relief, they should focus on revenue sources with the wherewithal to produce revenue over time. Unfortunately, the tobacco tax hike proposed in an amendment 603 to LB 170 not only would fail to be an enduring revenue source, it would risk worsening interstate trafficking of tobacco products.

Nebraska currently taxes a pack of cigarettes at $0.64. The LB 170 proposal hikes the tax to $1.36, a 112.5% increase, putting Nebraska’s tobacco tax in line with Iowa’s rate per pack. However, Missouri’s tax rate of $0.17 is a fraction of both Iowa and Nebraska’s tax rates.

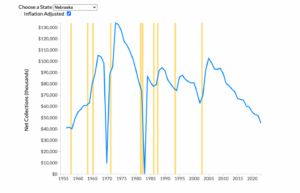

The tobacco tax increase is dedicated to Nebraska’s general revenue fund, indicating that lawmakers see it as a way to plug a budget gap, fund government services, or even fund a reduction in another tax. But tobacco taxes are an unreliable source of revenue for general services and tax relief. Consider the performance of tobacco tax revenue over time, as tracked by the Tax Foundation. Ever since the 1970s, an increase in rate (market by yellow) creates a short spike in revenue followed by a steep drop-off in revenue.

Such a volatile revenue source makes a weak basis for government funding and tax relief. Cigarette taxes are volatile because of the long-run trend of lower tobacco product use, along with the ongoing problem of cigarette smuggling.

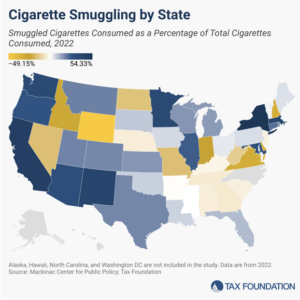

Cigarette smuggling is especially prevalent when there is a significant different in tax rates between two bordering states with population centers living near the border. Currently, Nebraska experiences low cigarette smuggling rates, with smuggling at only 2% of total cigarette consumption. However, that could change with the tax hike considered in the amendment to LB 170.

![]()

![]()

Wyoming and Missouri have among the highest rates of outbound smuggling in the country because of their low tax rates. Wyoming’s tax of $0.60 per pack is close to Nebraska’s current rate, and the border between the states is not highly populated. But a tax hike in Nebraska would nonetheless incentivize smuggling activity. However, the more pronounced smuggling risk is along the border with Missouri.

Missouri’s tax rate of $0.17 is not only a low rate, it is a low rate very near to Nebraska’s population centers. Missouri to Omaha is less than an hour drive, and it’s under 90 minutes from Missouri to Lincoln. If Nebraska moves its tax rate to $1.36, that creates a $1.19 arbitrage opportunity per pack of cigarettes. The arbitrage value of 50 cartons would be nearly $600. The well-established illicit trade in tobacco would fill this arbitrage gap, and would erode sales in Nebraska’s large metro centers.

While simply raising the tobacco tax raises risks, the amendment to LB 170 recognizes risk reduction strategies in taxation that are worth considering. Lower tax rates can be imposed on less harmful forms of nicotine and on products use to stop smoking as an overall harm reduction strategy. A risk-conscious approach to taxation makes sense, but simply raising the risk of smuggling through tax rate hikes does not.