Closing Nebraska’s $262 million Biennial Budget Gap

Platte Institute’s proposal to address the state’s $262 budget gap is to freeze the growth in two tax credit programs. The two-year freeze would yield $162 million in budget savings which, coupled with a $100 million draw down on the state’s rainy-day fund, would fix the issue for the current budget.

Going forward, lawmakers should use the interim to study the different forms of tax relief that have been provided by the state, double down on those that provide a better return-on-investment, and consider scaling back those that provide a less efficient return in tax relief.

To start, Nebraska faces a $262 million budget gap for the biennial budget. Platte Institute believes that the biggest driver of overspending has been the growth in subsidies for local government spending. Over the biennium, Nebraska state government will spend nearly $3.5 billion ($1.7 billion and $1.8 billion) out of the general fund for programs that subsidize local government spending. This data is provided in page 12 of the state’s budget book.

![]()

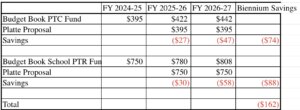

The largest transfers are the Property Tax Credit Fund (PTC) and the School Property Tax Relief Fund (SPTR), which accounted for $395 million and $750 million in the 2024-25 fiscal year. These are the two programs Platte Institute recommends freezing for the biennium, yielding $162 million in savings from freezing rather than growing the credit programs. The chart below displays the annual and cumulative savings from freezing the programs at 2024-25 levels.

Platte’s recommendation is not without precedent, and would give the legislature time to review the efficacy and affordability of these rapidly-growing credit programs. For example, Nebraska lawmakers skipped an entire year of funding the school property tax relief credit program for taxes paid in 2024, resulting in legislative proposals to find $637 million in funding to plug the ‘missing year’ of credits from 2024. Platte’s proposal, in contrast, is to simply freeze the credit programs at record-high levels – higher, in fact, than the levels when lawmakers skipped a year.

Lower Efficiency in Tax Relief

The PTC and SPTR credit programs provide less efficient tax relief than other forms of tax cuts because they do not address the true source of high property taxes, which is local government spending. Instead, they provide an offset reduce the pain of local government spending without fixing the root of the problem.

In fact, the credit programs create a “third-party payer problem.” The state wants property tax relief, but the state does not stop local governments from rapidly raising spending. Thus, the credit programs can incentivize faster local government spending growth because local officials can point to the credits as a state-provided offset to their local spending decisions. As a result, a dollar provided into the credit programs does not cleanly translate into a dollar of property tax relief because some of that tax relief is “consumed” by the local government through greater spending.

In contrast, income tax cuts provide perfect dollar-for-dollar tax relief. Lower rates result in fewer dollars owed to the state. In addition, the income tax cuts themselves restrain state spending by slowing the growth in a major state revenue source. Thus, income tax cuts are more efficient, restrain state spending, and make Nebraska more competitive.

Even within property tax relief programs, there are better options to put “lead on target.” For example, the state is in the process of eliminating the community college property tax and taking over the funding of community college. This approach eliminates the “third-party payer” problem because the state becomes the payer. The local property tax for community colleges is removed, tax payers get the relief of tax elimination, and there is not a risk that local governments will use the state subsidies to offset their spending growth. The same efficiency in tax relief could be achieved by eliminating the smaller property taxes for educational services units (ESUs) and tangible personal property (TPP). The state could eliminate these taxes altogether.

In contrast, the credit programs do not restrain local spending and thus provide a lower return-on-investment per dollar of state tax relief funding.

Cash Sweeps

Lawmakers are considering $160.4 million in cash sweeps to balance the budget in contrast with Platte’s proposal to save $162 million by freezing the growth in spending on large tax credit programs. Platte prefers to focus on balancing the budget through restraint in spending rather plugging a budget gap with one-time funds. The rainy-day fund is the appropriate source of any one-time funds to plug a budget gap, and Platte supports utilizing these funds to finish closing the gap after exercising spending restraint.

Cash sweeps should be analyzed to see what programs they would impact and whether they need to be repaid later. But overall, sound budgeting requires a structural gap to be fixed with structural solutions rather than one-time cash infusions.

Platte looks forward to supporting lawmakers and Governor Pillen in their work to provide the best outcomes for Nebraskans.